Looking for Lower-Cost, Flexible Health Coverage?

If you’re self-employed, healthy, or frustrated with high premiums and deductibles,

private health membership plans may be a better fit.

These plans aren’t part of the ACA Marketplace — they’re independent health programs that combine preventive care, cost-sharing, and concierge-style support at a fraction of traditional insurance costs.

Explore Your Options

You can enroll in either of our trusted membership programs year-round.

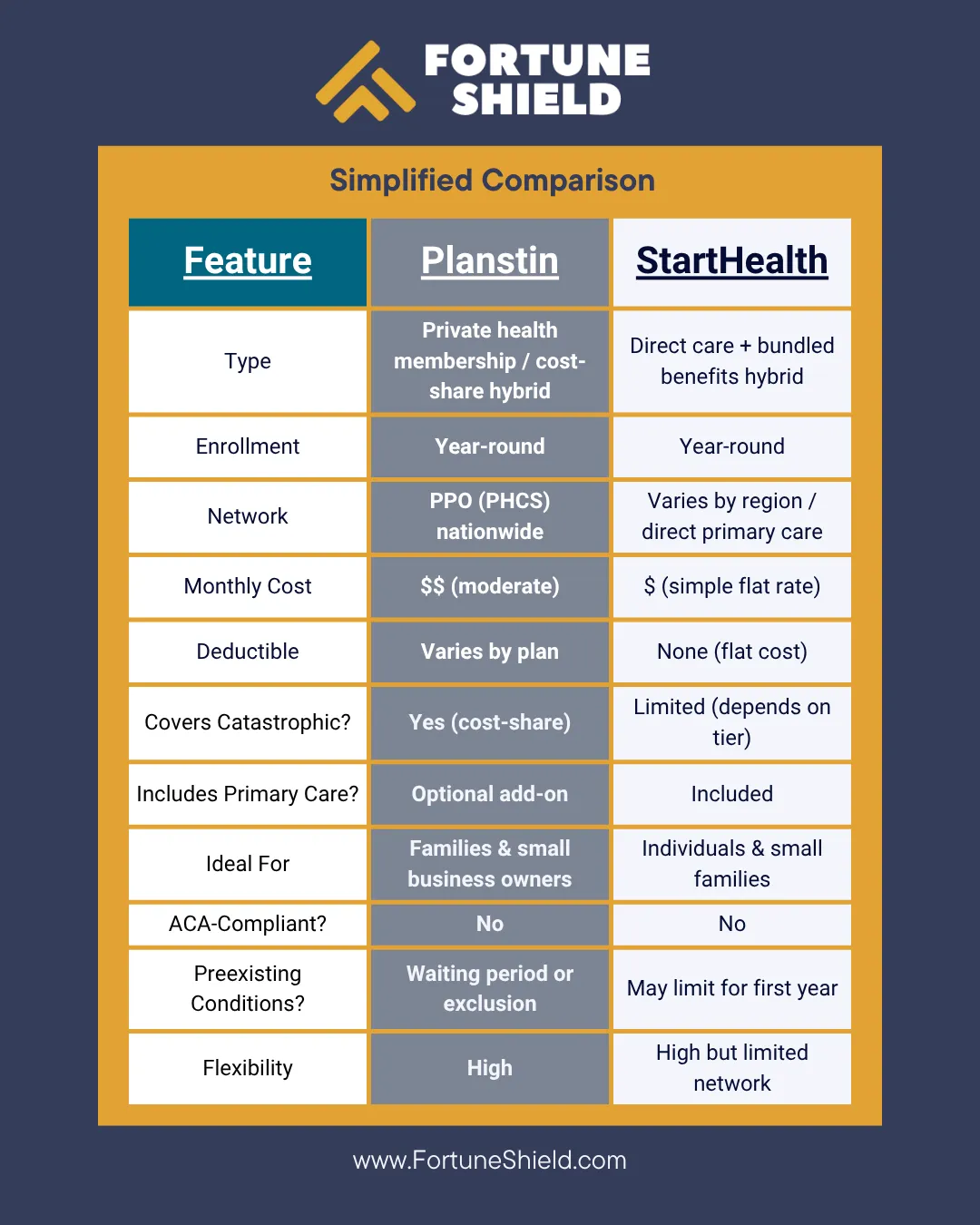

Planstin Health

Planstin is a private membership-based health program that blends:

A PPO-style network (via PHCS or similar)

Access to direct primary care

A health cost-sharing component for major medical needs

It’s not ACA-compliant insurance — it’s a medical cost-sharing membership with administrative support and optional add-ons (e.g., dental, vision, telehealth).

Best for:

Self-employed individuals, small business owners, or families who rarely use healthcare but want protection for big events

Healthy individuals frustrated by ACA costs and high deductibles

Households over ACA income limits (not eligible for subsidies)

People comfortable managing some out-of-pocket costs before major needs

Potential Drawbacks:

Not ACA-compliant: may lack certain “essential health benefits” (maternity, mental health, etc.)

Medical underwriting applies: preexisting conditions may be excluded for a period (usually 12–24 months)

Variable reimbursement: cost-sharing programs aren’t legally required to pay every claim (though reputable ones usually do)

Limited preventive coverage: depends on chosen tier

No subsidy eligibility: you pay full monthly membership

Strengths:

Lower monthly costs (30–60% less than ACA)

Year-round enrollment

PPO-style access to nationwide network

Concierge-style support and member advocacy

Limitations:

Not considered insurance under ACA

Preexisting condition limitations

No federal subsidy assistance

Must be comfortable with a membership structure, not a guaranteed claim payer

StartHealth

StartHealth is a direct care membership model with bundled benefits — combining primary care, diagnostics, and catastrophic coverage into one predictable monthly cost.

It’s a newer hybrid between direct primary care and cost-sharing/indemnity plans.

Best for:

Individuals or families wanting simplicity and predictability

Members who want one monthly payment that includes primary care, labs, and imaging access

Healthy people tired of deductible confusion and network restrictions

Those who want a clear digital experience (app, portal, telehealth)

Potential Drawbacks:

Limited nationwide reach (newer program): provider access varies by region

Not ACA-compliant: does not satisfy the ACA minimum essential coverage rule

Limited catastrophic cap: some tiers have lower maximum protection than traditional major medical

Out-of-network or specialty care may require coordination through StartHealth’s partner network

No tax subsidies: out-of-pocket cost, though often cheaper overall than unsubsidized ACA plans

Strengths:

Flat, transparent pricing (no deductible)

Includes direct primary care and telehealth

Great digital experience

Year-round enrollment

Limitations:

Newer company, smaller network footprint

Not ACA-compliant (membership model)

Limited catastrophic caps depending on tier

Not eligible for federal subsidies

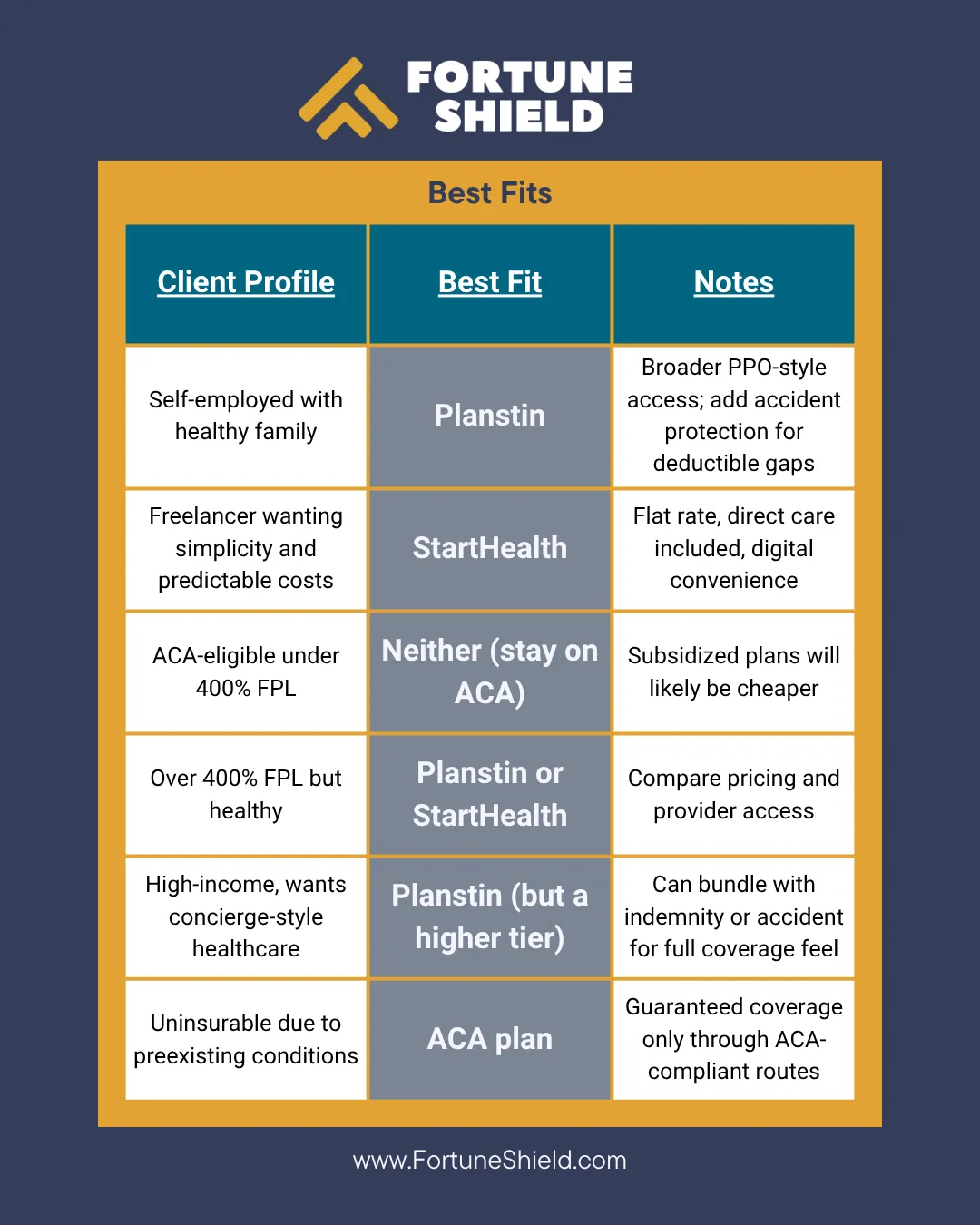

Which Plan is right for me?

Both options offer flexible, affordable alternatives to traditional health insurance —

but the right fit depends on your lifestyle, health needs, and budget.

Not sure which option is best?

Our licensed agents can walk you through both programs and help you find the most cost-effective plan for your situation.

Fortune Shield is a licensed, education-first protection resource. NPN: 1073776. Not all products are available in all states. Eligibility and benefits vary by carrier and state. Enrollment subject to approval. Fortune Shield is not connected with or endorsed by the U.S. government or the federal Medicare program.

© 2026 Fortune Shield | All Rights Reserved

Site Created by Design Logic Agency